“New” After-Tax Contributions Offer Greater Savings,

More Flexibility

After-Tax Contributions a “Back-Door” to Roth

After-tax contributions are nothing new. Ironically enough, your plan may have had after-tax contributions at some point, but they went by the wayside during a document restatement cycle or an amendment.

A newer strategy for after-tax contributions is using them in the retirement plan to allow high earners (or high savers) to not only save more than the regulatory limits allow them on pre-tax and Roth contributions, but to also convert their after-tax dollars to Roth and then enjoy the benefits of tax-free earnings (hence the name, “back-door” as it’s a way around the IRS limits). This allows individuals to get significantly more dollars into a Roth account.

Let’s take a closer look at how this works.

Understanding Contribution Limits

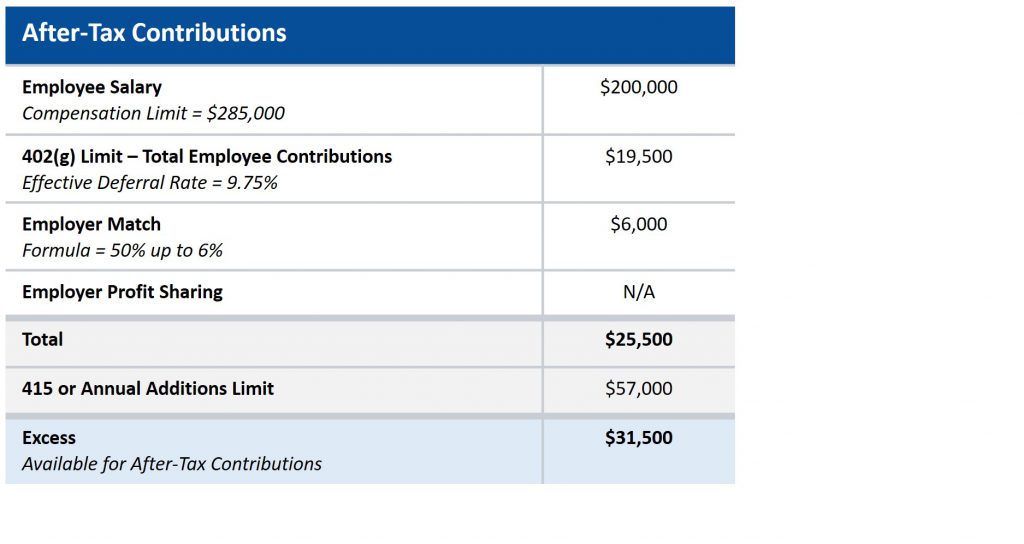

When we think about after-tax, we must separate it from what we know of the standard 402(g) limit contributions, i.e.: traditional pre-tax and Roth after-tax (for 2020 that combined pre-tax and Roth limit is $19,500). After-tax contributions have a different structure. They are included in the Annual Additions or 415 limit (for 2020 that is $57,000).

Here is an example of what a hypothetical employee’s after-tax contribution would look like:

Note that we are disregarding the allowed $6,500 catch-up contributions. Those can be made via pretax or Roth contributions and are added on top of the Annual Additions Limit.

Mechanics of After-Tax Contributions

Now that we know how much we can contribute in the form of after-tax, what do we do next?

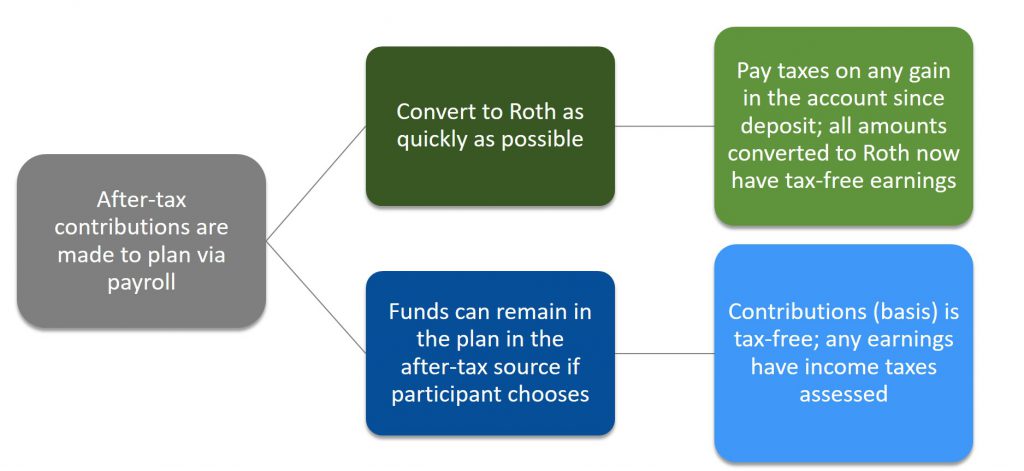

First, we must confirm the retirement plan allows for Roth in-plan conversions. This ensures we can convert these after-tax contributions to Roth so that we have the benefit of tax-free earnings.

The Roth in-plan conversion process can vary significantly depending on your recordkeeper/provider. In theory, however, as soon as the after-tax contribution money enters the account, those funds are immediately converted to Roth.

If the funds sit in an account, even for a few days, there will be taxes (ordinary income) due on any gains at the time of conversion. Any losses to the principal will also reduce the amount converted.

After-Tax Contributions Process

Testing Considerations for Plan Sponsors

So, this seems easy enough; what’s the catch? From a plan sponsor’s standpoint, back-door Roth contributions can be a bit of an administrative headache.

After-tax contributions are tested as part of the Average Contribution Percentage (ACP) test, not the Average Deferral Percentage (ADP) test. Furthermore, Safe Harbor plans do not get a testing pass – the ACP test still needs to be run. If testing fails, after-tax contributions are refunded. Top-heavy testing will also need to be conducted. Larger organizations with diverse salary levels will not (usually) have any significant testing issues, but smaller organizations will want to run through some scenarios with their consultant prior to implementing this plan design feature.

If your plan committee has testing concerns, there are a few things you can do:

- Consider putting a limit on the after-tax dollars that can enter the plan; for example, $10,000 per participant.

- Limit the number of Roth conversions allowed per participant per year to force employees to be strategic about their contributions in order to avoid significant tax hits.

- Encourage non-highly compensated employees to contribute on an after-tax basis and treat those funds as an emergency fund within the plan. The after-tax contributions can be withdrawn at any time and in the meantime can be invested. Remember, however, that the earnings will be taxed.

What to do next

While the process to incorporate after-tax contributions includes some hoops to jump through, it can be worth it for certain organizations, allowing employees to put away significant amounts of money for retirement.

To understand if it’s right for your organization, consider the advantages and disadvantages:

Advantages:

- Your executives and other high savers will appreciate this option

- It can be a nice recruitment and retention tool for talent

- When used correctly, it is a great retirement planning strategy

- The emergency savings aspect of after-tax contributions is especially relevant as employers seek ways to support their employees’ financial wellbeing

Disadvantages:

- It’s confusing for the average plan participant

- It must be coupled with education, which depending on your providers, can be an extra cost.

- It could potentially adversely affect the plan’s testing, resulting in refunds.

Allowing after-tax contributions is an advanced plan design feature. Understanding its complexity requires experts familiar with plan administration and testing implications. The team at Francis Investment Counsel has in-house expertise built over decades of working closely with plan sponsor clients and leaders in the recordkeeping industry. We’ll help you evaluate your retirement plan design and determine the best process forward. Reach out to us directly or fill out the form below to get started.

Tags: after-tax contributions, after-tax, Roth, back-door